Beer as a mirror

With the fall of the beer cartel, Switzerland’s breweries entered a new era. The way was clear for foreign corporations, alternative business models and smaller competitors. This phenomenon reflects the history of an entire national economy.

Nemo Krüger

Nemo Krüger is studying economic history at the University of Zurich and works as a research assistant for the project “The Mass Politics of Disintegration”.

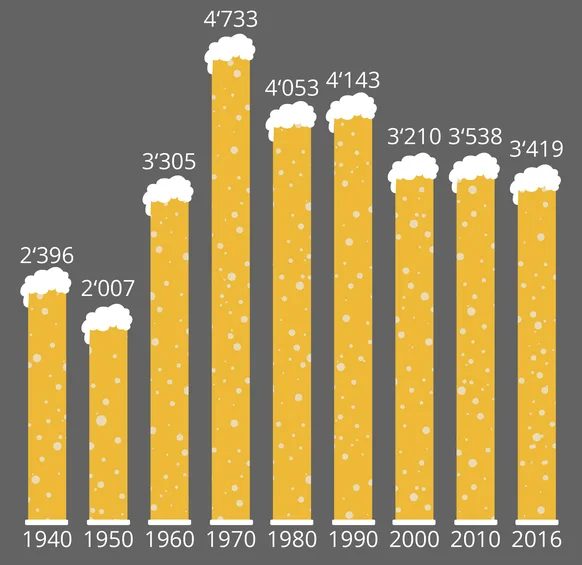

Competition in the beer industry was severely restricted. In 1935, the breweries had agreed to abandon their costly rivalry – and they had mostly stuck to the agreement ever since. By signing the convention, the members of the Swiss Brewers’ Association promised to stop poaching each other’s customers. They standardised their beer, and advertising was financed collectively by the association’s members from then on. In collaboration with the publicans’ association, they even worked out a system for “resale price maintenance”. The breweries standardised not only their own sales prices, but also the prices at which the beer was sold to customers.

The beer industry was not an isolated case. Most manufacturing companies in Switzerland were involved in agreements of one sort or another. No one made a secret of it: in a 1957 investigation, the Federal Price Formation Commission described Switzerland’s economy as “organised down to the last detail”. Around two-thirds of the trade associations investigated were involved in cartel agreements.

Despite the ideal of a free market economy, the cartels were generally tolerated. In 1954 the LdU, a political party which was associated with Migros, launched an initiative “against the abuse of economic power”. The initiative was rejected in 1958, with 74 per cent of votes against. In the notes relating to an initial, toothless antitrust law, in 1961 the Federal Council lauded the possibility of “removing or mitigating excesses of competition by private channels”.

Lost protection

There was a marked “trickle-up” effect: between 1970 and 2005, the share of employment in Switzerland’s domestic industry fell from 33 to 15 per cent, and its contribution to value creation fell from 27 to 13 per cent. Under the pressure of the strong franc, globalised production capabilities and sluggish growth, Switzerland changed from a manufacturing to a service economy.

Survival strategies

The beverage giants were in good company. Since the 1990s, Switzerland has mutated into a mecca for multinational companies. In 2019, more than 16,000 companies had their headquarters in the Alpine republic, with another 14,000 operating branches. Measured on the basis of direct investments made abroad by Swiss companies, since 1995 no country has been more closely interconnected with the world than Switzerland.

Under the very descriptive name REG Real Estate Group, in 2004 Hürlimann-Feldschlösschen merged with PSP Swiss Property AG, making it the largest real estate firm in Switzerland. Since 2011, an upmarket spa has been installed on the former Hürlimann site in the heart of the city of Zurich. Next door are the offices of Google, another multinational. The site of Winterthur’s Haldengut brewery is now graced by modern apartment buildings, and there’s a hip pop-up bar on the roof of the old main building. Sponsor: Heineken.

Localness, for the few

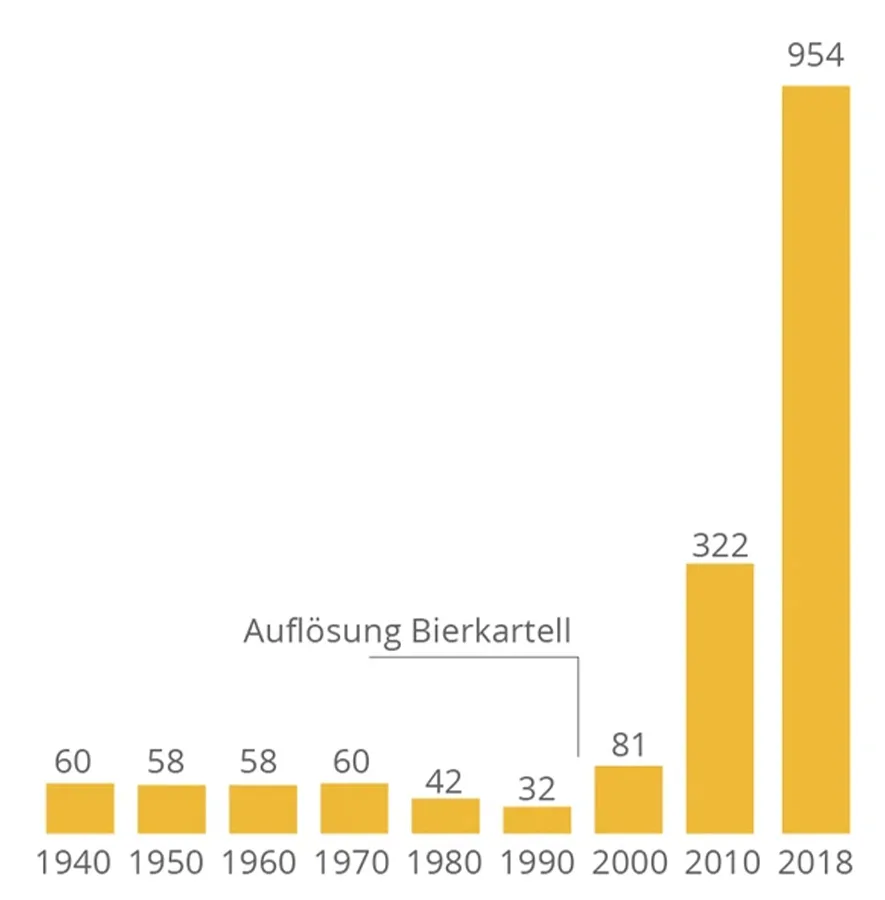

A third category of producers also formed: the microbreweries. Since the end of the cartel, their numbers have really exploded. Over intervals of ten years, the 31 Swiss breweries became first 92, then 345 and, in 2021, 1,278. Sophisticated craft beers started to compete with lagers that all looked and tasted the same. The logic of standardised industrial production had given way to a need for uniqueness and individuality, the mass product of scepticism towards corporations and globalisation. But the “too big to fail” momentum of the microbrewing scene lagged behind its goals. The beer market remained dominated by corporations. Even now, Heineken and Carlsberg split around 70 per cent of the output, and the regional breweries another 25 per cent. The others are doing battle for the rest: more than 1,000 beer makers are fighting it out over 1 percent of the market share.